Skip to Content

Skip to Content

How to Claim Lost Wages After an Injury

Lost wage compensation is the legal right to recover income you missed because someone else’s negligence left you unable to work. Whether your injury came from a car accident, a slip and fall, or a workplace incident, the process to claim lost wages after injury follows the same core logic: document your financial loss, link it directly to your injury, and submit a well-supported demand. Insurers and courts require proof, not just your word. That means medical records, employer verification, and wage calculations that hold up to scrutiny. Get these right from the start, and your claim stands on solid ground.

What documentation is required to prove lost wages after injury?

Strong documentation is the foundation of every successful lost wage claim. Without it, even a legitimate injury can result in a denied or reduced payout. Insurers are trained to look for gaps, and a single missing document can give an adjuster reason to question your entire claim.

The core documents you need include:

- Employer verification letter: A letter on official company letterhead confirming your job title, hourly or salary rate, and the exact dates you were absent. Formal employer verification strongly supports your claim’s validity with insurers and is far more credible than an informal note or email.

- Pay stubs: At least 3 months of pre-injury pay stubs establish your income baseline. They show your regular earnings, overtime patterns, and any bonuses or commissions you typically received.

- Medical records with specific restrictions: Your doctor’s notes must explicitly connect your injury to your inability to perform your job duties. Vague instructions to “rest” are routinely rejected by insurers as voluntary absence, not a compensable work restriction.

- Documentation of lost benefits: If your employer contributed to your 401(k) or paid a portion of your health insurance, those contributions stopped when you stopped working. Gather statements showing those amounts.

- For self-employed claimants: Tax returns averaged over 2–3 years, Schedule C filings, and detailed income statements replace the employer letter. Self-employed claimants often need forensic accountants to reconstruct income and separate business expenses from personal costs.

Pro Tip: Ask your physician to write a note that names your specific job title and lists the physical or cognitive tasks you cannot perform. A note that says “patient cannot lift more than 10 pounds or stand for more than 20 minutes” is far stronger than one that says “patient should avoid strenuous activity.”

The difference between a paid claim and a denied one often comes down to whether your medical records speak directly to your work restrictions. Generic documentation leaves room for doubt. Specific documentation closes that door.

How to calculate your lost wages claim including bonuses and benefits

Calculating your lost income accurately is not just about multiplying your hourly rate by missed days. A complete claim captures every income component that stopped because of your injury.

| Employment type | Calculation method | Key documents needed |

|---|---|---|

| Hourly employee | Hourly rate × missed hours | Pay stubs, employer letter, time records |

| Salaried employee | Annual salary ÷ 260 workdays × missed days | Pay stubs, employer letter |

| Self-employed | Average net profit over 2–3 tax years ÷ workdays × missed days | Tax returns, Schedule C, income statements |

| Commission-based | Average monthly commission over prior 3–6 months × missed months | Pay stubs, commission statements |

Lost wage claims can include base salary, lost bonuses, commissions, overtime if a consistent pattern exists, and lost benefits like 401(k) matches and employer health contributions. Overtime is only recoverable if you can show a documented history of working those extra hours, such as five additional hours every week for the prior six months.

Benefits are the most commonly overlooked component. If your employer paid $400 per month toward your health insurance and $200 per month toward your retirement account, those amounts belong in your claim. Add them to your total economic loss calculation.

Pro Tip: Pull your last three years of W-2s alongside your pay stubs. The W-2 captures total compensation including bonuses and employer-paid benefits that may not appear on individual pay stubs. This gives you a complete picture of what you actually earned.

Common mistakes that undervalue claims include ignoring lost benefits, failing to document overtime history, and using gross pay instead of total compensation. Each of these errors leaves real money off the table. Understanding how total economic loss is calculated gives you a clearer picture of what your claim is actually worth.

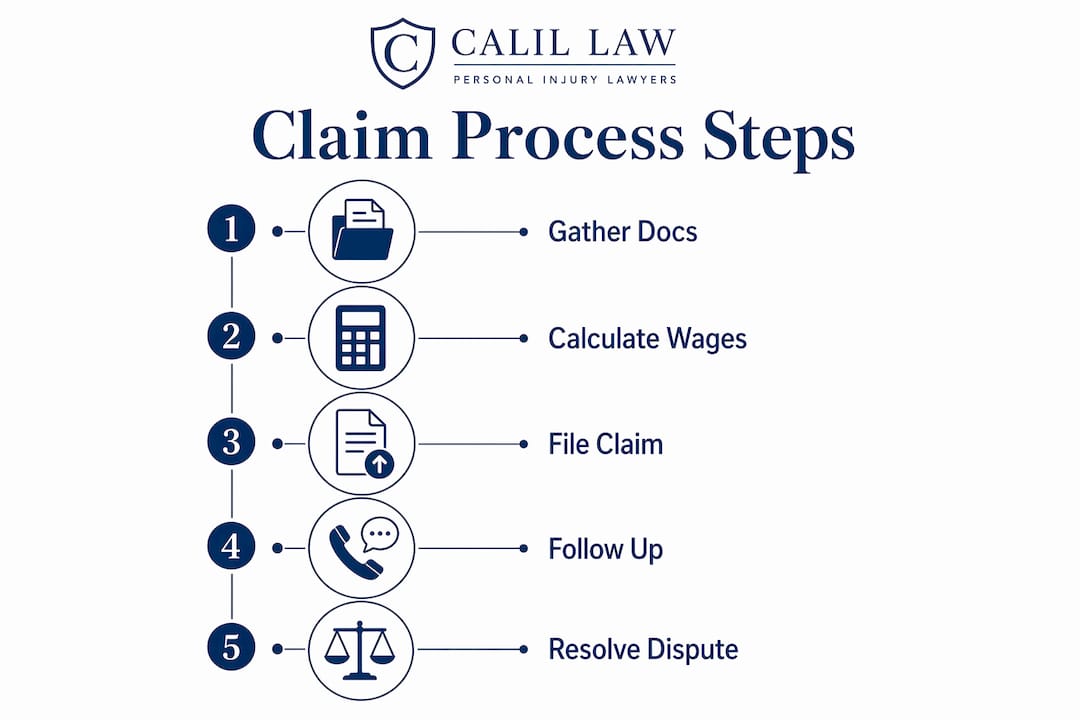

How do you file a lost wage claim with an insurer?

Filing your claim correctly is as important as documenting it. A disorganized submission gives adjusters an easy reason to delay or deny your request for wage loss after accident.

Follow these steps in order:

- Compile your complete claim package. Gather your employer verification letter, at least three months of pay stubs, medical records with specific work restrictions, and your wage loss calculation with all income components itemized.

- Draft a formal demand letter. State your total economic loss clearly, including the dates you missed work, your income rate, and every component of your claim. A formal demand letter sent to the insurer with medical records, employment verification, and detailed wage loss calculations initiates the recovery process.

- Send by certified mail. Sending demand letters by certified mail provides proof of delivery and establishes the start of the claim timeline. This creates an audit trail if the insurer later claims they never received your submission.

- Track every communication. Log the date, time, and content of every phone call, email, and letter. Note the name of every adjuster you speak with.

- Know your deadlines. Claims involving government entities may require notices within 90 days of the injury. Missing these deadlines can bar your claim entirely, regardless of how strong your documentation is.

When your claim involves a no-fault insurance policy, you submit directly to your own insurer first. Third-party liability claims go to the at-fault party’s insurer. The documentation requirements are the same, but the process and timelines differ. Understanding how accident compensation is determined helps you set realistic expectations before you submit.

If your claim is denied or delayed, request the denial in writing. A written denial gives you a specific reason to address, and it creates a record you can use if you escalate to litigation.

Common challenges when dealing with insurance adjuster pushback

Insurance adjusters do not work for you. Their job is to resolve claims at the lowest possible cost. Knowing their tactics in advance puts you in a stronger position to protect your claim’s value.

The most frequent challenges you will face include:

- Demanding exact medical linkage. Adjusters require that your medical records explicitly connect your injury to your specific job duties. Medical notes must link specific limitations caused by the injury to the claimant’s job duties to be valid. A note that does not name your occupation or describe your physical work requirements gives the adjuster room to argue you could have worked.

- Challenging self-employed income. Adjusters routinely dispute self-employed claims without clear, professionally analyzed financial data. Without a forensic accountant’s report, your income reconstruction is easy to dismiss.

- Invoking the duty to mitigate. Claimants have a duty to mitigate losses. Refusing suitable light-duty work or failing to seek alternative employment can legally reduce your compensation. If your doctor clears you for desk work and your employer offers it, declining that offer weakens your claim.

- Delaying responses to wear you down. Prolonged delays are a negotiating tactic. Maintain your paper trail and respond to every request in writing.

Self-represented claimants often receive undervalued settlements because incomplete or weak documentation gives adjusters the opening they need to minimize payouts. An attorney or forensic accountant changes that dynamic by producing documentation that is difficult to dispute.

When your claim is complex, particularly if you are self-employed or your income includes multiple components, hiring a personal injury attorney before you submit your demand letter reduces the risk of leaving money on the table. Early legal consultation helps identify missing documentation and realistic claim valuation, even if you ultimately handle the claim yourself.

Key Takeaways

Recovering lost income after an injury requires specific medical documentation, accurate wage calculations, and a properly filed demand letter sent before key deadlines expire.

| Point | Details |

|---|---|

| Documentation is the foundation | Gather pay stubs, an employer verification letter, and medical records with specific work restrictions before filing. |

| Calculate every income component | Include base pay, overtime history, bonuses, commissions, and lost employer benefit contributions in your total claim. |

| File formally and on time | Send your demand letter by certified mail and meet all deadlines, including 90-day notice rules for government entity claims. |

| Know the duty to mitigate | Refusing available light-duty work can reduce your compensation; follow your doctor’s return-to-work guidance carefully. |

| Get legal help early | An attorney or forensic accountant strengthens documentation, improves claim valuation, and reduces the risk of a lowball settlement. |

What I’ve learned about lost wage claims after years in the courtroom

The biggest mistake injured people make is treating their lost wage claim as an afterthought. They focus on their medical treatment, which is right, but they forget that the financial side of their case requires just as much discipline and documentation.

I have seen strong injury cases settle for far less than they were worth because the claimant could not produce a clear wage history. A vague doctor’s note and a few pay stubs are not enough. The insurer’s adjuster will find every gap in your records and use it to argue that your losses were smaller than you claim.

Litigation is a tool, not an automatic step. A well-documented demand letter resolves most cases without a lawsuit. When litigation is necessary, it gives you access to evidence through discovery and produces a collectible judgment. But the best outcomes I have seen came from clients who arrived with organized records, specific physician notes, and a clear calculation of every dollar they lost.

Self-employed claimants face the hardest road. Their income is harder to prove, and adjusters know it. If you run your own business, bring in a forensic accountant before you submit your claim. That investment pays for itself many times over.

My advice is simple: consult an attorney early, even if just for one meeting. You will learn what your claim is actually worth and what documents you still need to gather. That knowledge alone changes the outcome.

— Jorge

Calillaw is ready to fight for your full recovery

Recovering the wages you lost because of someone else’s negligence is your legal right. The process is detailed, and the stakes are real.

Calillaw’s personal injury attorneys have spent decades building and litigating exactly these kinds of claims in Florida. The firm handles everything from straightforward wage loss calculations to complex self-employed income reconstructions. Calillaw works directly with clients to gather the right documentation, build a complete demand, and negotiate from a position of strength. When insurers push back, the firm pushes harder. Contact Calillaw today for a free case evaluation and find out what your claim is actually worth.

FAQ

What counts as lost wages in a personal injury claim?

Lost wages include base salary, hourly pay, overtime with a documented history, bonuses, commissions, and lost employer-paid benefits like health insurance contributions and 401(k) matches. Every income component that stopped because of your injury belongs in the claim.

How do I prove lost wages if I’m self-employed?

Self-employed claimants use tax returns averaged over 2–3 years, Schedule C filings, and detailed income statements to establish an income baseline. A forensic accountant can reconstruct income and separate business expenses to produce credible claim data.

What happens if my doctor’s note is too vague?

Vague medical notes that say only “rest” or “avoid strenuous activity” are routinely rejected by insurers as evidence of voluntary absence rather than a compensable work restriction. Your physician must name your specific job duties and list the physical limitations your injury creates.

How long do I have to file a lost wage claim?

Deadlines vary by state and claim type. Claims against government entities may require written notice within 90 days of the injury. Missing a deadline can bar your claim entirely, so confirm the applicable statute of limitations with an attorney as soon as possible.

Does refusing light-duty work hurt my claim?

Yes. Claimants have a legal duty to mitigate their losses. If your employer offers suitable light-duty work and your doctor approves it, refusing that offer can reduce the compensation you are entitled to recover.