Skip to Content

Skip to Content

How to Handle Insurance Bad Faith in Florida

Insurance bad faith is defined as an insurer’s unreasonable or dishonest refusal to fulfill its obligations to a policyholder. For Florida residents dealing with a denied personal injury claim, recognizing and knowing how to handle insurance bad faith can mean the difference between recovering what you are owed and walking away with nothing. Florida law, including the Florida Unfair Claims Practices Act and Fla. Stat. §624.155, gives you specific legal tools to fight back. The Florida Department of Financial Services oversees insurer conduct, and a formal process called the Civil Remedy Notice (CRN) is your first legal weapon.

What are common examples and signs of insurance bad faith in Florida?

Bad faith is not about whether the insurer was right, but whether their conduct was reasonable when handling your claim. That distinction matters enormously. An insurer can deny a claim incorrectly and still avoid bad faith liability, as long as they acted reasonably. The moment their conduct becomes unreasonable, dishonest, or deliberately obstructive, Florida law steps in.

The Florida Unfair Claims Practices Act imposes strict deadlines and standards for insurer conduct. Violations of those standards are the foundation of most bad faith claims. Knowing the warning signs early gives you time to build your case before evidence disappears.

Common examples of insurance bad faith conduct in Florida include:

- Unjustified denial. The insurer rejects your claim without citing a valid policy exclusion or factual basis.

- Lowball offers without methodology. Systematic lowball offers that lack any documented valuation process are a recognized form of bad faith.

- Unreasonable delays. Failing to acknowledge, investigate, or respond to your claim within statutory timeframes signals bad faith.

- Inadequate investigation. The insurer closes your claim without reviewing medical records, accident reports, or other submitted evidence.

- Misrepresenting policy language. The adjuster tells you a covered loss is excluded, citing policy language that does not actually say what they claim.

- Repeated document requests. Asking repeatedly for documents you already provided is a delay tactic, not a legitimate investigation step.

Pro Tip: Keep a written log every time an adjuster calls you. Note the date, time, name, and exactly what was said. Oral promises and verbal denials disappear. Your written record does not.

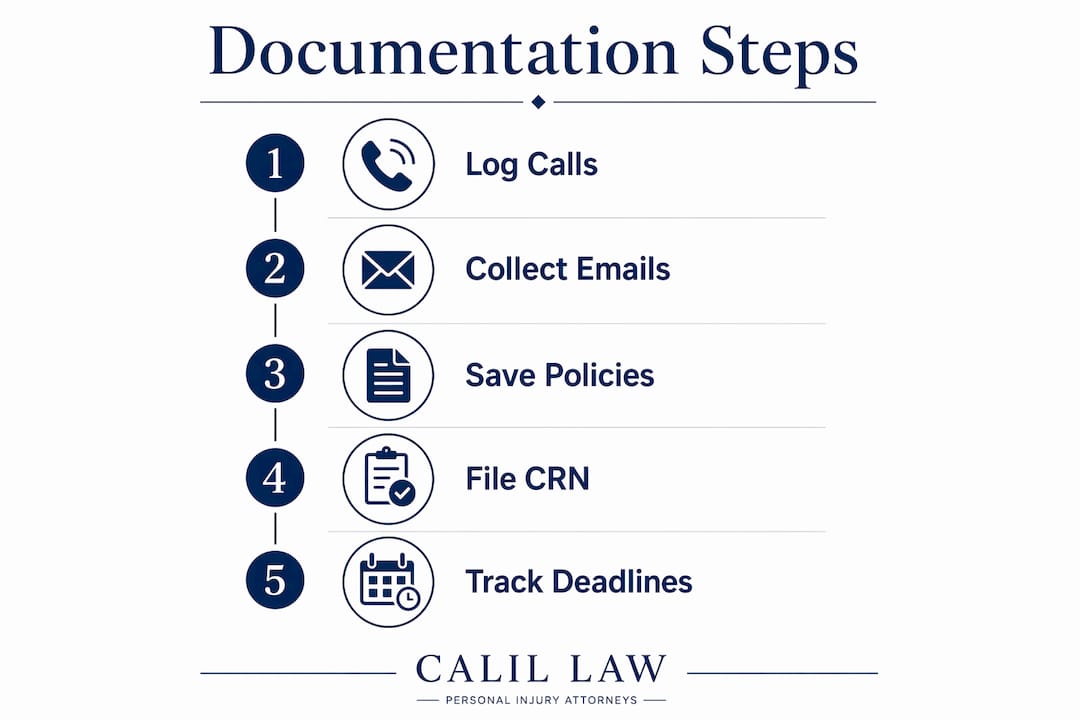

What documentation do you need to build a bad faith claim in Florida?

Building a bad faith case requires proving the insurer lacked a reasonable basis and acted objectively unreasonably. That proof lives in your documentation. Without it, even a clear case of misconduct becomes difficult to prove in court.

Florida’s Civil Remedy Notice (CRN) has strict content requirements. You must describe the specific statutory violation, the facts supporting it, and the damages you suffered. Errors or omissions in the CRN can invalidate your entire bad faith claim before it reaches a courtroom.

The table below outlines the core documentation types, their purpose, and best practices for collecting them.

| Documentation Type | Purpose | Best Practice |

|---|---|---|

| Chronological communication log | Proves timeline of insurer delays and responses | Record every call, email, and letter with dates and names |

| Copies of submitted claims and evidence | Shows what the insurer received and when | Send all documents via certified mail and keep receipts |

| Missed internal insurer deadlines | Demonstrates statutory violations | Compare insurer response dates against Florida’s required timelines |

| Written denial letters | Identifies the stated reason for denial | Request all denials in writing; never accept verbal denials only |

| Civil Remedy Notice (CRN) filing confirmation | Satisfies Florida’s mandatory pre-suit requirement | File through the Florida Department of Financial Services portal and save confirmation |

| Policy documents | Establishes coverage terms the insurer must honor | Obtain a full certified copy of your policy at claim inception |

Florida law under the Prompt Payment of Claims Act requires insurers to acknowledge a claim within 45 days and pay or deny it within 90 days. That means you can measure insurer conduct against a concrete legal clock. Missing those deadlines entitles you to penalties and attorney fees.

Pro Tip: After every phone call with an adjuster, send a follow-up email summarizing what was discussed. Write something like: “Per our call today, you confirmed X.” This creates a written record the insurer cannot later deny.

How do you legally handle insurance bad faith claims in Florida?

The legal process for pursuing a bad faith claim in Florida follows a specific sequence. Skipping any step can forfeit your rights entirely. Filing a Civil Remedy Notice with the Florida Department of Financial Services before filing a lawsuit is not optional. It is a mandatory condition under Florida law.

Here are the required legal steps, in order:

- File the Civil Remedy Notice (CRN). Submit the CRN to the Florida Department of Financial Services, identifying the specific statutory violation and the facts supporting it. This must be done before any bad faith lawsuit is filed.

- Allow the 60-day cure period. After the CRN is filed, the insurer has 60 days to correct the violation. If they cure the problem within that window, the bad faith claim may be extinguished. If they do not, you have grounds to proceed.

- Send a policy-limit demand letter. A clear demand letter supported by documentation triggers bad faith exposure if the insurer ignores it. Include medical records, bills, and a reasonable deadline for response.

- Consult a Florida bad faith attorney. The procedural requirements are technical. An attorney familiar with Florida bad faith claims can identify violations you may have missed and protect your rights going forward.

- File the bad faith lawsuit. If the insurer fails to cure and negotiations break down, your attorney files suit under Fla. Stat. §624.155 or §626.9541, depending on the type of insurer involved.

- Pursue discovery of the internal claim file. Obtaining the insurer’s internal claim file during litigation can reveal adjuster notes, reserve valuations, and internal approvals that expose the insurer’s true intent. This evidence often makes or breaks a bad faith case.

Understanding how compensation is determined when a lawsuit is filed against an insurer helps you set realistic expectations before you enter litigation.

What mistakes should you avoid when disputing bad faith insurance?

Most bad faith claims fail not because the insurer was innocent, but because the claimant made procedural errors that handed the insurer an easy defense. Proper procedural compliance and detailed logs are the foundation of every successful bad faith claim in Florida.

The biggest mistake is relying on verbal conversations with adjusters. Adjusters are trained communicators. What they say on the phone and what appears in the claim file are often two different things. Every significant communication must be confirmed in writing.

Pro Tip: Track every statutory deadline on a calendar from the moment you file your claim. Florida’s personal injury statute of limitations and the CRN filing window are unforgiving. Missing either can end your case.

Dos and Don’ts for handling a bad faith insurance claim:

- Do send all communications in writing, including follow-up emails after phone calls.

- Do file the CRN through the Florida Department of Financial Services before taking legal action.

- Do keep copies of every document you submit, with proof of delivery.

- Do consult an attorney before accepting any settlement offer.

- Don’t rely on verbal promises from adjusters about coverage or payment timelines.

- Don’t miss the CRN filing deadline. A missing or defective CRN invalidates your bad faith claim.

- Don’t sign any release without understanding what rights you are giving up.

- Don’t ignore repeated requests for documents, even if you have already provided them. Respond in writing and note that the documents were previously submitted.

What compensation can you recover for insurance bad faith in Florida?

Bad faith insurance claims can recover damages far beyond the original unpaid claim amount. Florida law allows recovery of consequential damages, attorney fees, statutory penalties, and in egregious cases, punitive damages. That scope of recovery is what gives bad faith claims their real leverage.

Fla. Stat. §624.155 and §626.9541 are the primary statutes governing bad faith remedies in Florida. Under §624.155, if an insurer fails to settle a claim in good faith and an excess verdict results at trial, the insurer can be held liable for the full amount of that verdict, even if it exceeds the policy limits. That exposure is significant and often motivates insurers to settle once a properly filed CRN is in place.

Attorney fees are recoverable under Florida’s bad faith statutes. That means pursuing a bad faith claim does not require you to pay legal fees out of pocket if your attorney works on contingency. The financial barrier to fighting back is lower than most claimants realize. Legal representation also maximizes your recovery. Attorneys experienced in insurance claim disputes know how to use discovery, demand letters, and litigation strategy to extract full value from a bad faith case.

Key Takeaways

Successfully handling an insurance bad faith claim in Florida requires early documentation, a properly filed Civil Remedy Notice, and strict compliance with Florida’s statutory deadlines before any lawsuit can proceed.

| Point | Details |

|---|---|

| Bad faith defined | An insurer’s unreasonable conduct, not just a wrong decision, triggers bad faith liability under Florida law. |

| CRN is mandatory | Filing a Civil Remedy Notice with the Florida Department of Financial Services is required before any bad faith lawsuit. |

| Document everything | Chronological logs, written denials, and certified mail receipts form the backbone of your bad faith case. |

| Statutory deadlines matter | Florida’s Prompt Payment of Claims Act gives insurers 45 days to acknowledge and 90 days to pay or deny a claim. |

| Recovery goes beyond the claim | Florida bad faith victims can recover consequential damages, attorney fees, penalties, and excess verdict amounts. |

What I have learned from Florida bad faith cases

After working with clients across Florida who faced stonewalling, lowball offers, and outright denials on legitimate personal injury claims, one pattern stands out clearly. Insurers rarely commit bad faith in a single dramatic act. They do it gradually, through delays, repeated document requests, and vague communications that erode a claimant’s resolve over months.

The claimants who succeed are the ones who started documenting from day one. Not after the denial. Not after the third delay. From the very first phone call. By the time a bad faith case reaches litigation, the insurer’s internal claim file often tells a story the adjuster never intended to share. Reserve figures set far below the claim value, internal notes questioning coverage without legal basis, and approval chains that show deliberate delay. Discovery of that file changes the dynamic of the case entirely.

My honest observation is that most claimants underestimate how much procedural compliance matters in Florida. The CRN requirement is not a technicality you can work around. It is the gate. Miss it, and the insurer wins on procedure before the merits are ever argued. Get it right, and you hold real leverage.

Stay persistent. Insurers count on claimants giving up. The ones who document carefully, file correctly, and get experienced legal support are the ones who recover what they deserve.

— Jorge

How Calillaw supports Florida bad faith and personal injury claims

Calillaw is a Florida litigation firm led by a Board Certified Civil Trial Lawyer with decades of courtroom experience in personal injury and insurance disputes. When an insurer denies or mishandles your claim, Calillaw provides the legal strategy and advocacy to hold them accountable.

Calillaw handles bad faith insurance claims on a contingency fee basis, meaning you pay nothing unless your case resolves in your favor. The firm reviews your claim, identifies statutory violations, and manages the CRN process from filing through litigation if necessary. If you are facing a denied or delayed personal injury claim in Florida, contact Calillaw for a free case review. Your rights have a deadline. Acting early protects them.

FAQ

What is insurance bad faith in Florida?

Insurance bad faith in Florida is defined as an insurer’s unreasonable or dishonest conduct in handling a policyholder’s claim. Florida law under Fla. Stat. §624.155 gives claimants the right to sue insurers who fail to settle claims in good faith.

What is a Civil Remedy Notice and why does it matter?

A Civil Remedy Notice (CRN) is a mandatory pre-suit filing submitted to the Florida Department of Financial Services before a bad faith lawsuit can proceed. Failing to file a proper CRN invalidates the bad faith claim entirely under Florida law.

How do you prove bad faith against an insurance company?

Proving bad faith requires showing the insurer acted objectively unreasonably, not just incorrectly. Evidence includes chronological communication logs, missed statutory deadlines, lowball offers without methodology, and the insurer’s internal claim file obtained through discovery.

What damages can you recover in a Florida bad faith claim?

Florida bad faith claimants can recover the original unpaid claim amount, consequential damages, attorney fees, statutory penalties, and excess verdict amounts above policy limits. Punitive damages are available in cases of egregious insurer conduct.

How long do you have to file a bad faith claim in Florida?

The CRN must be filed before the statute of limitations on the underlying claim expires. Because Florida’s personal injury deadlines are strict, consulting an attorney as soon as bad faith conduct appears is the safest course of action.